Banks, Borders, and Bitcoin in Africa

Why an L3 in Africa, pegged to Bitcoin, running through the Lightning Network disrupts everything

NOTE: This piece is based off of a concept and platform that we thought to build and integrate with Moja a year ago and then put aside.

One of the advantages of building out the largest public WiFi network in Africa (Moja WiFi) is that we learned a lot about how ordinary people think and what they want. As you would expect, after people get onto WhatsApp to chat and watch a couple YouTube videos, their next question is “how do I make money with the internet?” There is this desire to figure out how to be part of the global 21st century economy, to see if there is more money that can be made than from connecting with the rest of the world than just what they have available locally.

Across the continent we have underemployment, so people hustle and try to make the most of what they have. Everyone’s an entrepreneur, and everyone needs to keep as much of the money that they make as they can.

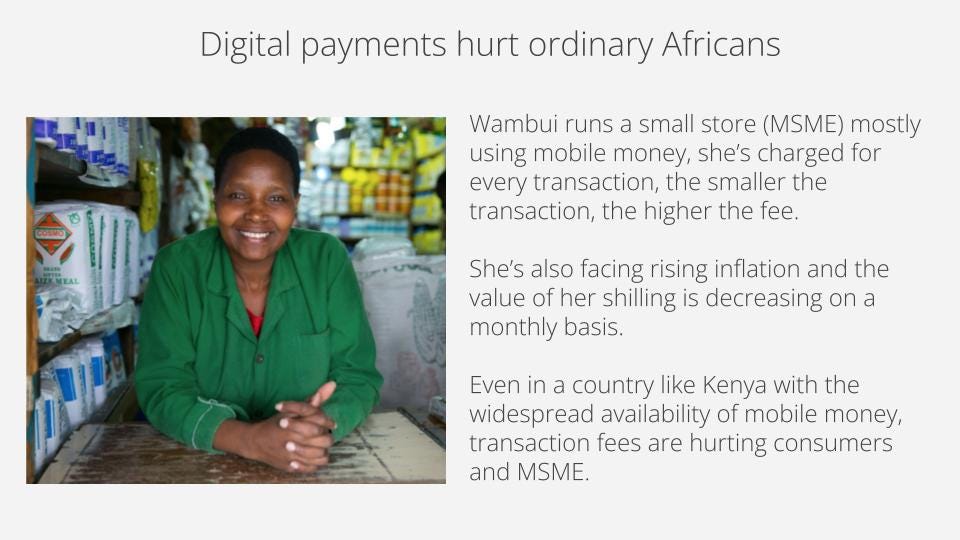

Banks are expensive.

Mobile money is expensive.

Taxes are expensive.

It was this realization, mixed with reading and researching a great deal on Bitcoin and other crypto that opened up some new ideas. Without going through the exhaustive replay of that, suffice it to say that I believe the long-term win will be pegged to Bitcoin and not other cryptocurrencies.

New Rails Needed

With a youth-bulge leading to well over one billion people, 66% of which are unbanked, carrying 300 million smartphones, and split up amongst 54 countries; this is both a big market with many gatekeepers AND an incredible opportunity to create something that changes the fabric of the economy on the continent. Politics and trade won’t fix this for the everyday citizen, a technological solution is necessary, one that increases wealth and becomes the lodestone for everyone to use, which creates its own network effect and opens the doors to further innovations in digital finance.

What we need is a cross-border platform for people in Africa to earn digitally, buy and sell physically, and send money to each other. This should be fast, cheap, and easy, but today it’s not. Consumers struggle with the friction and cost of the banking and mobile money systems which are further exacerbated by country-level taxes and restrictions making it impossible for average Africans to become part of the global digital economy.

Most entrepreneurs and investors are looking at this as a “moving money” problem - as seen by large investments in mobile money aggregators (Flutterwave $170m raised), remittance (Sendwave $500m acquired), or fintech payment platforms (Opay $400m raised). These are valuable, but they only address one aspect of the underlying issue. These products don’t adequately address the real world issues of “how do I earn?”, “how do I build wealth?”, and “how do I avoid the poverty-tax of transaction fees?”. In addition, users need the ability to seamlessly transact between the digital and physical world through a network of merchants and agents.

It is abundantly clear that Africans want access to global crypto markets. Three of the top 10 countries in the world whose citizens hold Bitcoin as a percent of GDP are Kenya, Nigeria, and South Africa. According to Chainalysis, Kenya is the #1 country globally for peer-to-peer crypto transactions. Nigerians, despite the government’s ban on crypto, still eclipsed more than $2B Bitcoin transactions in May 2021 alone.

Unfortunately, the complexity of traditional crypto transactions is too cumbersome and expensive for everyone other than the richest and most sophisticated traders. Other efforts at exposing consumers to the crypto markets have relied upon complex applications and risky exchanges that often attempt to avoid regulations.

Enter the 3rd Layer

Everything needs a name, so we’ll call this third layer Kado (short for “kadogo”, which means “small” in Swahili).

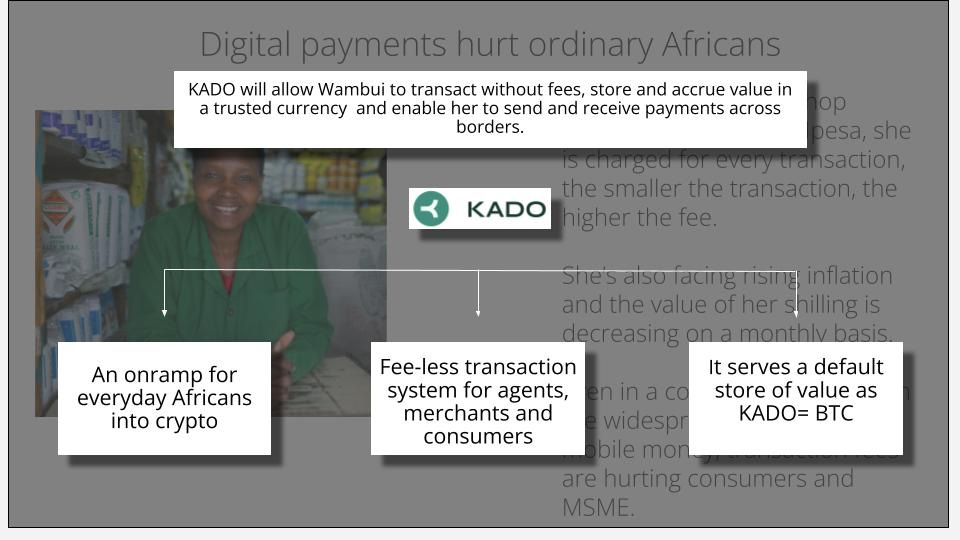

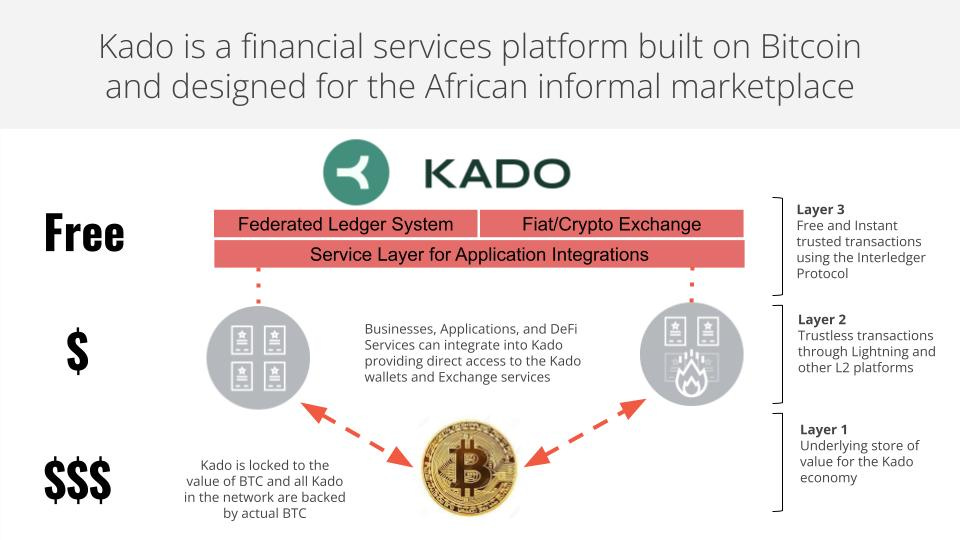

Kado is a Bitcoin-based financial services platform designed to work within the challenging social, political, and economic realities of Africa. It is built around a three-layer architecture that holds crypto assets at the treasury tier, allows for trustless transactions for businesses/merchants at the enterprise tier, and enables fast/free ledger-based transactions at the consumer tier. This means that consumers can earn, save, and spend an on-platform digital currency that is backed by the value of the underlying crypto assets and can be transacted instantly without transaction fees.

Businesses, merchants, and agents are able to seamlessly move funds between the platform currency (Kado) and external currencies including digital and fiat. This enables businesses to pay for digital work and merchants to receive payments within the Kado network without burdening consumers with the friction and cost of current financial systems. Kado will facilitate the integration of digital financial transactions into the lives of everyday Africans allowing them to earn, buy, and sell without boundaries.

While some of these functions can be accomplished with existing digital currency solutions, the challenge in emerging markets is that the technical complexity, costs, and transaction settlement times are prohibitive hurdles for most consumers. Exacerbating this situation is that many African governments are either actively or passively anti-crypto. This innovation in digital financial services enables:

Everyday people to earn, pay for services, and trade peer-to-peer instantly and without fees

Local merchants to sell products, services, and exchange Kado for fiat currency.

How it Works

The Kado platform uses a three tier financial topology to achieve the maximum combination of security and transactional performance for all marketplace participants while keeping the cost of doing business to an absolute minimum. The underlying store of value within the marketplace is Bitcoin. This serves as the foundational currency that backs all of the higher order transactions within the network.

Businesses within the marketplace are able to utilise well established Layer 2 (L2) sidechain technologies like the Lightning Network to transact their Bitcoin without the time or cost of mainchain (Layer 1) settlement. This gives businesses the flexibility to keep operational float in a sidechain that allows for fast and inexpensive transactions while still ensuring the security of their underlying financial assets.

The final layer of the Kado platform is the marketplace’s own internal ledger system. This ledger system utilises a federated transaction authority to create instant financial transactions that can be handled at scale. Users are able to earn, buy, sell, and trade Kado instantly across the marketplace and still have the assurance that their Kado have concrete value in the foundational Bitcoin layer. The Kado platform can handle billions of micro-transactions across the various participants in the network allowing for both business and consumers to trade freely and then settle their Kado to the L2 sidechain and ultimately directly to the Bitcoin mainchain.

Value of a Kado

Although Kado are only maintained within the Kado ledger system, their fixed relationship to Bitcoin means that users can always see the current value of Kado in Bitcoin or fiat equivalents. This also means that individuals can choose to denominate P2P transactions in Kado and pay for the exchange of goods and services through a P2P transfer function. This same ability also serves as a basis for merchants to accept Kado for the sale of physical goods knowing that the value is well established and that the Kado are directly convertible into fiat or crypto. The Kado platform allows both merchants and consumers to seamlessly settle their Kado onto the L2 sidechain and from there they can be withdrawn as Bitcoin or exchanged for fiat.

Kado Agents

While buying Bitcoin for use on the L2 sidechain can be accomplished through a number of existing exchanges, it is anticipated that most Kado users will not have the sophistication to interact with crypto platforms directly. While Bitcoin can be purchased and then locked to the Kado L3, the primary means of converting fiat into Kado will be through agents. Much like the agents that provide cash in/out services for M-Pesa and other mobile money platforms, Kado Agents will be able to maintain a float of Kado that they can exchange for cash (mobile or physical) and also pay out cash for Kado received from a user. This mechanism will be an extension of the P2P transfer that is optimised for agents.

Summary

While the ideals of Bitcoin would seek to make every person on Earth an equal participant in the global marketplace, the reality on the ground is that many users lack the power, connectivity, and technical sophistication to be an active participant. Further, the costs of transacting directly on the Bitcoin mainchain are prohibitive for small transactions and users in emerging markets need to transact at exceptional small values - particularly relative to their counterparts in developed markets.

While the fee structure for using a sidechain like Lightning does improve the transactional economics, Kado is intended to go one step further and enable micro-transactions going both to and from the consumer giving maximum economic empowerment to even the least sophisticated consumer. Finally, with core partners providing critical community infrastructure such as connectivity and power, the Kado platform ensures that everyone has the ability to transact in this new world even if they can’t afford a data bundle or an hour of phone charging.

Final Note: A year later and I’m on the fence for this being a platform play, mainly due to centralization of a what is sure to be a disruptive solution. I now wonder if it could be done in a more federated way on that L3 layer (Kado) and thereby have more resiliency. Maybe it’s as simple as taking the open source, decentralized wallet design like the Web5 one by Block and using that mixed with Fedimint.