Barrels of Electrons... The Oil Equivalent of Bitcoin Mining

A barrel of oil vs. a megawatt of river power... which builds more wealth?

Run‑of‑river hydro sites in Africa, plugged into Bitcoin mining as an always‑available buyer, can beat the long‑term profitability of a productive oil well, creating decades of high‑margin, non‑depleting energy revenue that simultaneously powers local development.

I wrote this essay to prove to you that this type of energy development in Africa is a more sustainable and longer-lasting equivalent to oil production. In short, it’s a better investment. And, by using Bitcoin to monetize Africa’s vast hydroelectric potential, developers like Gridless can unlock Exxon-level energy economics while bringing electricity and opportunity to underserved areas.

[This essay is by my business partner Philip Walton, be ready to nerd-out on some numbers]

A few weeks ago Erik shared a clip from Landman where Billybob Thorton’s character is complaining about the environmental costs of producing wind and solar. His summary is that if the economics really made sense, then all of the big oil companies would certainly put all of their money into producing energy this way instead of the more perilous method of extracting energy from the ground.

The clip was catchy and, during my last trip to the US, I decided to take the opportunity to watch the rest of the series. As I watched episode after episode of the drama in the West Texas oil patch, I started to realize that there is a lot more in common with the business that these landmen were building and the one that we are building with Gridless Energy. This thinking led me down a rabbit hole of trying to understand the economics of oil production and then to draw some correlations with our own efforts at producing energy in the wilds of Africa.

Now I won’t pretend for a minute that I’m an expert in oil production and I’m sure there are nuances to my comparison that would cause any good oilman to cringe. That’s fine. My objective isn’t to present an absolutely perfect analogous comparison but, instead, to recognize the commonality of aspects of our business from those that have made so many fortunes in the oil-rich areas of the world.

Energy Equivalence

To begin, I started by looking at the electricity energy equivalent of a barrel of oil - the standard unit of production and sale for the petroleum industry. One barrel of oil equivalent (boe) is equal to 1,620 kWh of energy. Since, on a certain level, energy is energy; we can at least accept that any form of energy can be measured in any other acceptable unit of energy measurement. So while electricity generally is measured in kWh (or its big brother the MWh), there is nothing inaccurate in measuring energy output of an electricity generation plant in barrels of oil. They are, after all, equivalent quantities of energy.

If we were to take a 1MW run-of-river hydroelectric generation site, this site would produce a daily volume of nearly 15 barrels of oil. (Assuming you don’t trust my math, 1,000 kW times 24 hours = 24,000 kWh per day of energy. 24,000 kWh divided by 1,620 kWh per barrel = 14.8 barrels of oil per day.) If I wanted to have a site that produced 100 barrels per day then I would need 7MW of generation capacity. Now, based upon my brief research, a single land-based well that produces 100 barrels per day is a pretty good money maker for the oil industry (roughly $6,000 per day in income).

So let’s look at the economic comparison between an oil well that produces 100 barrels per day and a 7MW run-of-river hydro site.

Exploration

Oil wells are generally placed in known oil fields. As much as everyone would like to believe they are just sitting on a pool of liquid gold, the truth is that there are very specific geographic features that make oil both likely and extractable. Even with some knowledge that an area is good for oil production doesn't necessarily mean that where you drill will have the right features to allow for efficient extraction. Oilmen have to call in geologists and other scientists to use whatever advanced technology they have at their disposal to try and make an educated guess as to whether a given site is viable for a new oil well. Just because the guess is educated doesn’t mean they are always right. There is always a risk that the oil company will invest the money to drill and then come up empty handed. This really sucks since more than half the cost of a well is in the drilling.

For run-of-river hydro, we also need very specific features for where we build our sites - there is no point in exploring hydro in the middle of the Sahara desert. Our job is a bit easier in that we are looking at energy resources that are above the ground and can be efficiently evaluated using available data sources (e.g. satellite images, land surveys, river gauging stations). The two primary factors that determine the energy production potential of a site are the volume of water and the elevation change between the water intake and the generation point (this is called the head).

As a quick example, 1 m3/s of water flow at a head of 100m will produce around 800kW of electricity (at 80% generation efficiency). 10 m3/s of water at a head of 10m will produce roughly the same amount of electricity.

A perfectly efficient (100%) turbine - which sadly doesn’t exist - would produce exactly 981kW - which, if you remember your physics, is the gravitational acceleration constant in m/s2. Since basic surveying tools can tell us with absolute accuracy the head potential of our sites, the only question we have as hydro developers is how much water is flowing. This number can be known at any point in time but, what we can’t know for certain, is the change to that flow over the course of the year or over many years as weather patterns change.

Where the oilman has to risk spending money on drilling a non-productive well, the hydroman has to risk unpredictable water flows over the course of time.

Thankfully, we also have our smart scientist and they can generally use a combination of historical flow data, historical rainfall patterns, and rain catchment areas to give us a pretty good indication of what variability we can expect from a potential site. This comes in the form of a probability curve that we can use to determine how big we want to build our generation facility. As an example, a site might have a 60% probability of having an average of 10MW of production capacity but a 90% probability of having 7MW. While we could build for the max potential, we at least have the option of reducing our capital investment to try and align the size of our facility with the highest probability of expected water flow.

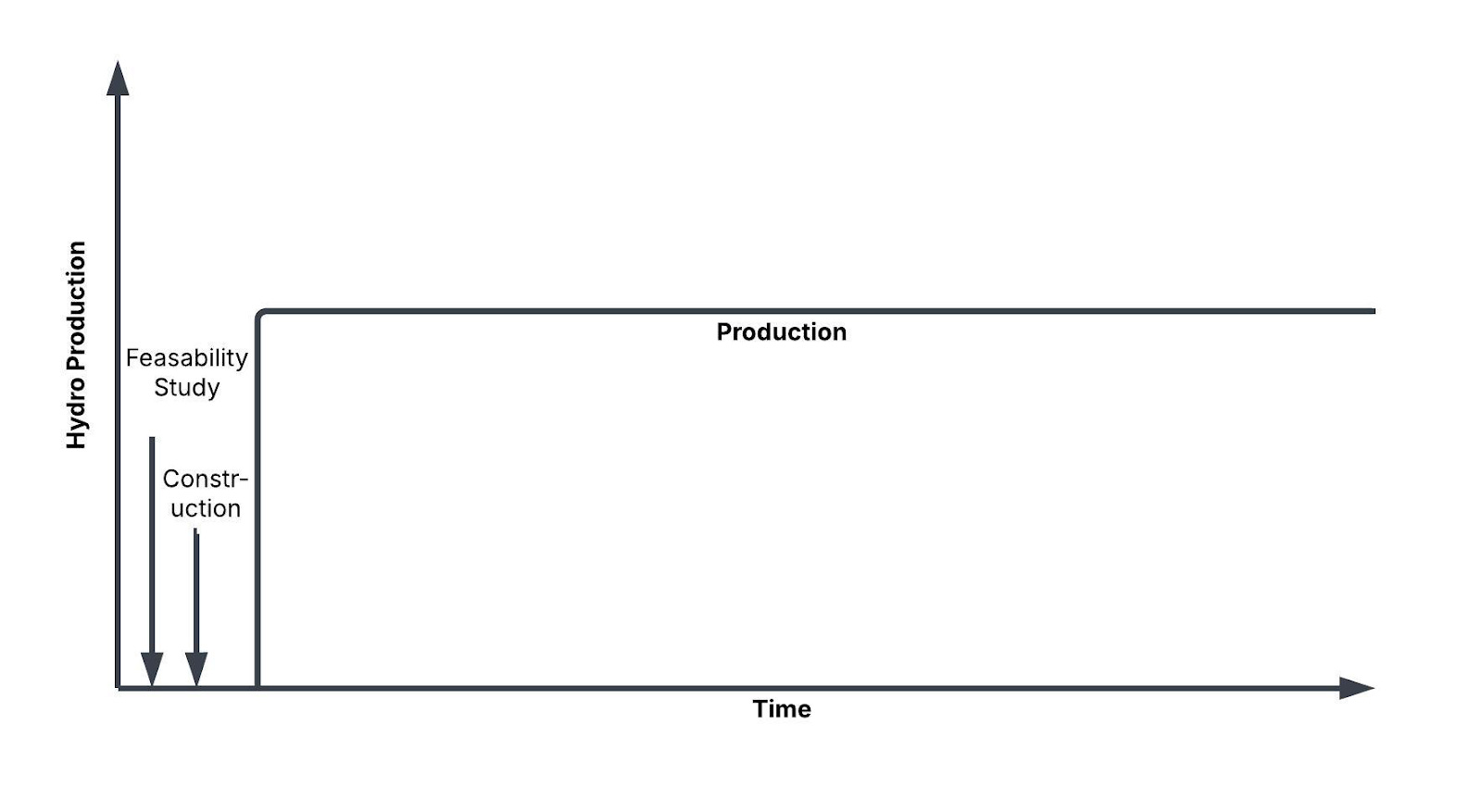

Production Lifetime

One of the key considerations for an oil well is that there is a finite amount of hydrocarbons in each pocket and eventually the well will go dry. This means two things for oil production, the first is that there is a finite (although not necessarily determinable) number of barrels of oil that can be produced and second the production of oil will decrease over time.

A 20 year production cycle for an oil well might look like this:

While there are sometimes opportunities to rework a well that will result in a restoration of some of the production capacity, there is no getting around the fact that ultimately the resources will be fully exhausted and there is nothing else to produce. Each well has a finite life.

Hydro, on the other hand, performs no extraction of a resource - it simply borrows the energy resource momentarily and then returns it to the river. While the lifetime of a hydro site may be impacted by climate changes and changes to upstream use cases such as agricultural extraction, the hydro itself has a net-zero impact on the amount of water flowing in the river. This means that a hydro site can run for 30, 50, or even 100 years (there are plenty of examples of sites this old) and continue to produce electricity because the resource is still available for generation.

A 30 year production cycle for a run-of-river hydro site might look like this (assuming an averaging of production over the various seasons):

Much like an oil well, a hydro site will require periodic refurbishment of components like turbines, bearings, and generators. However, the core infrastructure of a hydro site should easily outlast the lifetime of the developer if the site is properly maintained. This also means that older sites, on still viable rivers, can often be refurbished and restored to full production even if they have been sitting idle or underutilised for years. Climate or human forces may dictate that a given site eventually reaches a point of no longer being economically viable but the non-extractive nature of hydro energy generation means that it won’t be the producer that is driving these changes and these changes are not predictable nor inevitable like they are with oil production.

Cost of Production

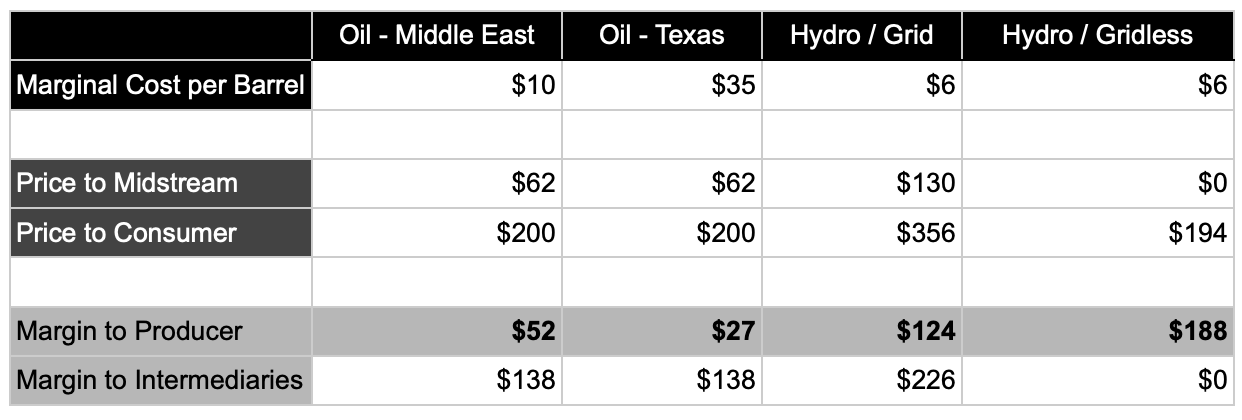

The oil industry has a much more complicated costing model than the hydro industry. Everything from the value of the mineral rights to the depth of the well can cause a particular project to vary wildly in terms of the overall costs. Like the hydroman, the oilman has to consider a combination of capital costs, financing costs, regulatory costs, operating costs, and overhead in determining their actual cost of production. All of these factors can then be aggregated and divided by the total lifetime number of barrels to give an oil producer an indicative break-even cost per barrel for a new site. If we look across the oil producing world, the break-even costs per barrel of production varies wildly from a little less than $10 per barrel in the Middle East to over $60 per barrel in Western countries. In addition to the cost of production, the oil producer also has to address the physical distribution of their output to a market point. This may be their own refinement facility or to a shipping point but, in either case, the market price per barrel is only realised at the point of sale. There could be a number of additional costs that will impact the overall economic performance of the facility even if it can produce cheap oil.

Hydro, like all forms of electricity production, uses a concept called the Levelised Cost of Energy (LCOE). This calculation is very similar to the break-even cost of production in oil with many of the same factors being considered. Fortunately, in the electricity space, the variability is a bit more limited than for oil but it is still cheaper to produce a kWh of electricity in most of Africa than it is to produce the same in N America or Europe. This is driven largely by the lower regulatory costs, lower labour costs, and the availability of abundant, renewable energy sources.

As an example, a 1MW solar plant in North America would produce power at an LCOE of $45/MWh ($0.045/kWh) and the same plant with the same costs would produce power at an LCOE of $35/MWh in Africa. Based on nothing but the difference in annual solar irradiation between these two geographies. This would result in break-even costs per barrel of $73 and $57 respectively.

A run-of-river hydro site in Africa would likely achieve an LCOE of $20/MWh or better resulting in a break-even cost per barrel of $32 or less. More importantly, once the initial investment is recovered on a run-of-river site - which can happen in less than 5 years, the marginal cost of production is around $4/MWh giving a cost per barrel of $6. By comparison, the marginal cost of production of a barrel of oil in the Texas Permian Basin is around $35 per barrel. This means that a typical hydro site in Africa will have an all-in cost lower than just the marginal cost of production in Texas. Once a hydro site is developed, the ongoing cost of production will be lower than the best oil producers in the world.

Energy Market

The sales markets for oil depend upon the type of oil extracted, proximity to an oil export point or processing centre, and transportation challenges between the point of extraction and the point of sale. Since oil tends to be concentrated in certain geographic regions, it is reasonable to build the infrastructure necessary to transport the extracted oil to market. In general, there are multiple organisations that each play a different role in getting a barrel of oil from the ground to your petrol tank. Upstream operators focus on the exploration and extraction of oil. Midstream operations take the extracted oil and move it to the point of refinement and processing. Downstream operators refine the extracted oil into usable products (e.g. transportation fuels, heating fuels, lubricants) that can then be further distributed to the final end consumer markets.

While this division of labour does create some operational efficiencies, it also results in economic inefficiencies as each player in this extended chain of production has to make money. As an example, a barrel of oil will produce about 73 litres of petrol and this represents about 46% of the total product volume output of that barrel. 73 litres of petrol at my local station in Kenya is currently $100. Assuming that is 50% of the economic value of the barrel then we can derive a total economic value of $200 per barrel at the end consumer. The current price (as of April 2025) for a barrel of Brent crude is $62. This means that $138 of value is being captured between production and the end consumer. Obviously a lot of that value gets distributed along the chain but it gives an end number to compare with our total economic output for electricity.

Electricity, like oil, has a physical constraint on distribution. From the point of generation to the point of consumption there must be an uninterrupted power line. In addition, there are transmission and distribution costs that come in the form of transformers, substations, transmission lines, connection points, etc. If we look at a typical independent generation site that is connected to a national grid in Kenya, they are getting paid around $0.08 per kWh and, as a consumer in Kenya, I am paying around $0.22/kWh. In oil barrel terms, the producer is receiving $130 per barrel and the total economic output is $356 per barrel. This is a similar ratio between production and end consumer as the oil industry.

While most independent power producers (IPP’s) strive to get a contract to sell 100% of their production to the national grid, some IPP’s go through the effort of building their own midstream/downstream operations and sell power directly to consumers. While this does allow them to capture more of the economic value it also severely impacts their overall ability to sell everything they produce since these local markets seldom have the economic capacity to buy all of the electricity. On one hand, they capture more value per unit of electricity, on the other hand they sell less units overall.

This issue of loss revenue changed radically in the early 2020’s when companies like Gridless demonstrated a model for connecting a networked energy market to stranded energy production regardless of where the production was taking place - including the remote areas of Africa. Bitcoin mining is, for all intents and purposes, an end consumer of electricity that requires no physical distribution infrastructure. The bitcoin mining machine is an adapter that connects an energy producer directly to a global energy market with just an internet connection.

This means that any energy producer can sell directly to a consumer market and bypass the entire midstream and downstream processes. Depending upon the efficiency of the mining equipment, bitcoin mining earns between $0.05 and $0.12 per kWh (38 J/T and 18 J/T respectively). This means that the oil barrel equivalent for bitcoin mining is $81 to $194 per barrel; at the point of production with no distribution costs other than a basic internet connection.

While an electricity consumer will always pay more than bitcoin mining, an IPP is now able to choose between two distinct markets for each unit produced and satisfy the higher paying market first before resorting to the lower paying market for any unsold units. This is the essence of the Gridless Energy model.

Gridless Energy vs Oil Production Equivalent

So what has made oil production such a key source of wealth over the last 150 years? In essence, it is the fact that there is an insatiable demand for the product and, once initial capex is invested, the asset continues to produce daily revenue for decades to come. Once an oil well is running, it is just an ongoing source of economic value - at least until it runs out. Countries, companies, and individuals throughout the world have radically transformed their economic futures based solely on their ability to cheaply produce barrels of oil.

Electricity generated from hydro is really no different and in many ways superior to oil production. We will never meet the ever-growing demand for electricity and, once the initial investment is made, a generation site will produce for as long as the energy resource continues to flow. With the advent of bitcoin mining we also now have market optionality that ensures that every unit of electricity produced has a ready and willing buyer.

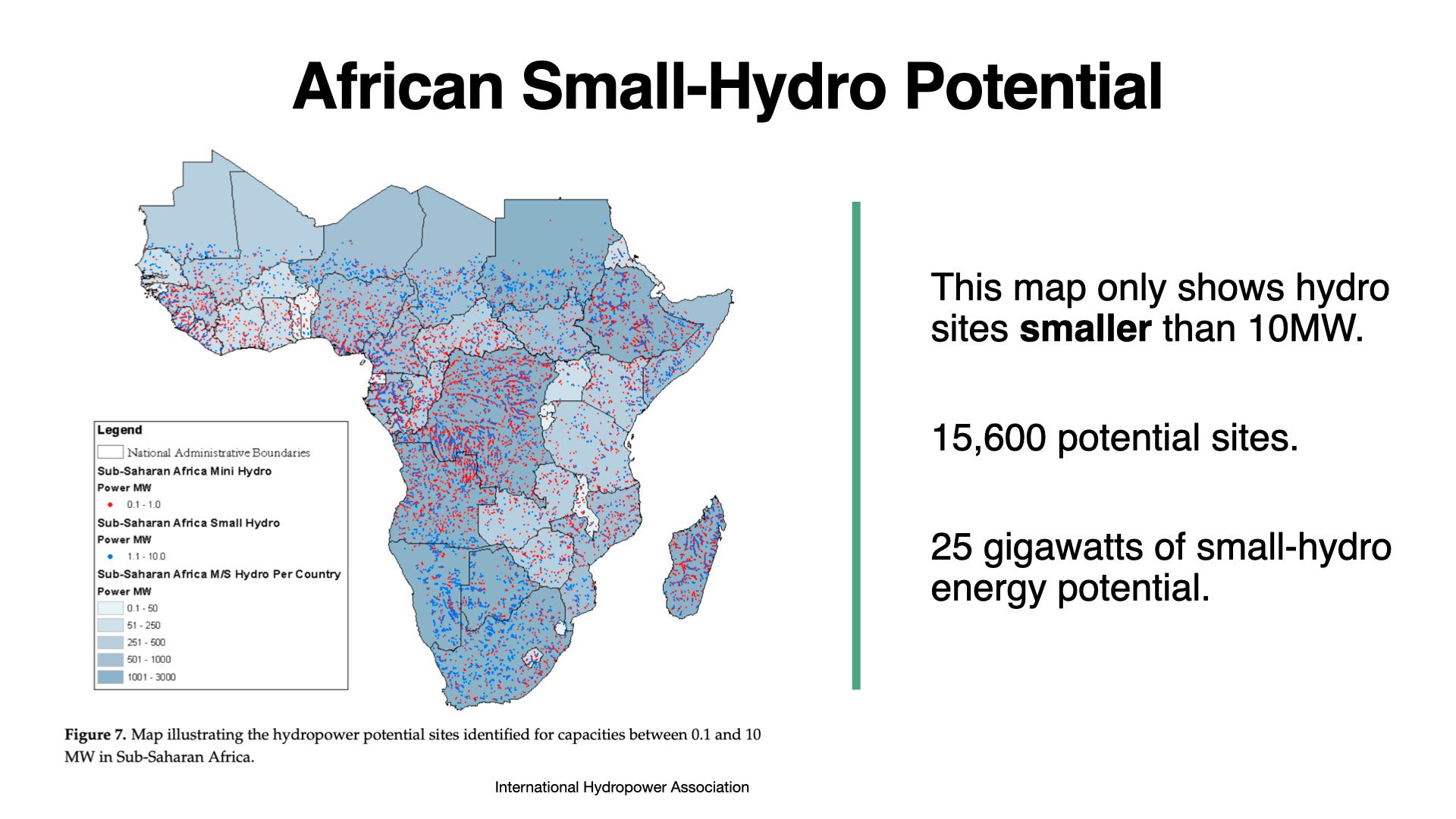

It is estimated that Africa has 400GW of hydro energy potential. In oil barrel equivalents that represents 6M barrels per day of production. This would place Africa’s hydro resources at 4th in the oil production list just behind the US, Saudi Arabia, and Russia. A little less than 300GW of new production would exceed the total production of the famous Texas Permian Basin that Billybob Thorton was fighting for in Landman - of which he had just a small piece. A little less than 50GW of new production would exceed the total energy production of the Basin’s largest oil company, Exxon. If we looked at it on a revenue basis, the Gridless Energy model would require only 9GW to match Exxon and on a gross margin basis, around 4GW.

There is an enormous opportunity to create generational wealth through energy development in Africa. Not just wealth for the investors and developers of this energy but, more importantly, for the communities that will benefit from access to this transformational economic driver. The cost of building a 7MW run-of-river hydro is around $15M and would produce $20K per day of revenue and $18K of gross margin. These numbers vastly improve upon the economics of oil exploration in almost every region of the world. Upwards of 50 years of daily revenue production 7x24x365 from an energy source that doesn’t get depleted and without impacting the source’s use for other purposes.

We have over 100 years of new bitcoin mining production remaining. We have that time (and most likely well beyond) to use this revolutionary monetary technology to make new energy development in Africa not just profitable but wildly profitable. Why would we not try and recreate the likes of Exxon, Aramco, Total, and others but without depleting our resources and instead building up the communities that are the furthest behind? There is a new energy boom coming and it is in Africa and it is driven by the power of Bitcoin to transform a continent that is desperately in need of economic transformation. Gridless is excited to be a pioneer in this new energy exploration and build a portfolio of energy producing assets that will contribute to the growth of progress of our amazing continent. Maybe one day the Gridless name will be listed with these other energy giants.